Atlas Engineered Products: Paying 1x Tangible Book Today for a Canadian Microcap with a History of Strong Growth

A unique roll-up opportunity coupled with yet another pandemic recovery story.

Disclosure: I am long AEP. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation, nor do I hold a position with the issuer such as employment, directorship, or consultancy. Content here does not constitute financial advice.

A bet on strong demand for Canadian construction building materials, AEP has grown revenue from $11 million to $37 million in three years but continues to trade below its reverse takeover price of $0.40 a share. At a current market cap of $21 million, you can buy the business today at almost no premium to tangible book value. While the story is imperfect, positive catalysts are aligning for a highly probable near-term outsized return.

Overview and Idea Selection

Atlas Engineered Products is Canadian national producer and distributor of prefabricated wooden building materials, such as roof trusses, walls with and without custom windows, joists, beams, and other components inherent to the wood frame dominated construction scene in Canada. AEP boasts a growing team of design architects, using Berkshire Hathaway owned MiTek’s building design software, creating custom solutions for both single family and multi-family residential.

AEP is best considered as roll-up with strong organic growth potential. The wooden engineered building materials segment is a boring, fragmented, and undercapitalized industry, marked by a preponderance of low technology enabled mom and pop shops with succession problems. AEP is currently the only nationally integrated supplier in Canada, providing a huge opportunity for selective and disciplined M&A activity. Many local markets are served by single suppliers making them quasi monopolies, as AEP currently is to Nanaimo and central Vancouver Island, both due to local permitting contexts and delivery economics.

AEP is based in Nanaimo on Vancouver Island, but operates six facilities across Canada. It came to my attention two years ago after a former professional acquaintance who I consider to be both highly competent and integrous joined to lead their local HR, providing me confidence about the quality of people involved. Clearly, I am exhibiting some local bias in this stock selection, however, having worked briefly in the Canadian construction building materials industry for Foundation Building Materials, as well as being the child of a business owner construction contractor father, this is well within my circle of competence to understand.

Further, this is a company has been hit hard by the pandemic. Construction overall has been delayed substantially across Canada due to material and labour shortages not to mention stop work orders and social distancing. Short term volatility in lumber prices has also wreaked havoc on margins. Both these phenomena are covered herein, with a focus on impact to working capital and lumber volatility on margins.

Two Years of Selected Data

After over three years as a publicly traded equity, AEP has struggled to return any value to its earliest shareholders. Dilutive acquisitions and slower than anticipated execution have seen impatient investors exit early for greener pastures. But after waiting patiently on the sidelines, I believe now is the optimal time to invest.

I expect revenues to rise to around $45 million for the year. While low profit margins continue to haunt the business, rapid revenue growth and improving fiscal discipline in operations could see AEP deliver upwards of $6 million in 2021 year-end EBITDA on a current market cap of only $21 million.

Price to Sales 0.55

Price to Book 1.6

EV/EBITDA 9.5

Profit Margin 3%

From current price of approximately $0.38 cents a share, my target price is $0.50 by year end 2021, representing approximately 30% upside. Of course, had one been watching this stock over the past year, numerous advantageous buying opportunities sub $0.30 have arisen of which, full disclosure, I have taken full advantage of.

I believe the market is mispricing AEP’s organic growth potential, however other factors are at play. A significant hangover of shareholders who purchased at inception have failed to see any returns and have been liquidating over the past year. As a young publicly traded microcap, there has been a tough learning curve for management, but with a maturing business model and a heightened focus on fiscal prudence, the risk/reward ratio is skewed to the upside.

Here is a checklist of reasons supporting my conviction on this thesis:

As an emerging quality business in contrast to established quality, expectations are unsubstantiated, giving ample room for near term above average returns should this thesis play out.

Growing capital turnover suggests future margin improvement is increasingly likely, but requires collection of past due receivables, which I believe is highly probable in the near term as pandemic disruption settles.

Recent lowering of fixed cost structure and leaner executive team even as revenue growth continues

Organic growth coupled with plenty of further M&A potential for productive assets at or below replacement value as evidenced by recent acquisitions

Founder/owner-operator run business with a shareholder aligned management team owning 17% of outstanding shares.

Sustainable debt with recent favourable refinancing in late 2020

Low price to sales offers uplift potential

Industry Levers

Private SME competition is fragmented and generally unable/unwilling to invest in production enhancing capex

Competition is aging out/fragmented and generally unable/unwilling to invest in automation/productivity enhancing capex

Unfinished product with potential to improve in multiple directions. Evidenced by recent innovation into prefabricated walls.

Strong consumer surplus evidenced by reduction in building costs through gains in efficiency by reducing labour inputs on site. Builders using AEP’s preassembled products are faster, more competitive and face less quality control problems.

Macro Levers

Hot Canadian housing market and chronic multifamily residential undersupply will see through continued demand for construction materials as population continues to grow; lowest number of housing units per 1,000 people of all G7 nations with that number set to see further decline with immigration

Chronic construction labour shortage will continue to reward AEP’s automation and prefabrication strategy

TAM growing swiftly, with a high probability that AEP becomes a share gainer, although this is difficult to track.

Risks

Scarcity of skilled construction labour impacts organic growth

Canadian housing market “bubble” bursts, unlikely given chronic secular undersupply

Poor M&A discipline, including issuing equity to fund acquisitions

General dilution: note that AEP raised $4.5 million February 2020 through a private placement deal of 11.5 million shares at $0.40 each

Entry of an irrational competitor

Lumber price volatility impacting margins

Estonian position exit

It is worth noting that AEP currently has over 17 million warrants outstanding at an exercise price of $0.60. 5,165,000 warrants were set to expire on October 31, 2020, and on December 3, 2020, but the company extended these warrants to October 31, 2021, and December 3, 2021, respectively. The remaining 12,148,019 expire on February 6, 2022.

Management clearly wants to see these warrants through as they offer a potentially lucrative source of capital for the company and given that they extended the goal posts for excise. These warrants do not present an immediate concern given the currently “low probability” of exercise. At the same time, with a cost basis significantly below the exercise price, I would be very happy to see shares gain enough to warrant the exercise of these warrants.

Management

CEO Hadi Abassi, a long time Vancouver Islander, acquired AEP in 1999 and grew revenues from $1-10 in 15 years. He knows the industry intimately and recognized the roll up opportunity amid industry fragmentation and the lack of clear exit opportunities for owners. Hadi stepped away from the reigns for a short period, while another CEO, Dirk Maritz was brought on in 2018. Maritz has since left, with Hadi back in the reigns as of February 2021. Hadi directly owns 5,587,386 shares while his family trust owns an additional 2,005,673. Hadi has never sold a single share.

Maritz was in briefly and never had substantial skin in the game as a shareholder. I think the idea was that a more veteran public company CEO might be able to give virgin AEP an edge, however this logic did not prove itself and I believe he was soon amicably pushed out by insiders.

In short, this is a founder/owner-operator run business with a shareholder aligned management team; management owns 17% of outstanding shares plus options, most of which expire at $0.60. Managers have also been purchasing new shares recently, while relatively small amounts, the CEO and two other directors all purchased shares as recently as June 2021.

The Baltic Connection

It is also worth noting that a consortium of Estonian funds is in control of about 9,500,000 shares which they purchased under a Private Placement Offering in October of 2018. They own an equivalent number of warrants with a strike price of $0.60, effectively controlling more than half of the float of existing warrants. The Baltic region is one of the world largest lumber and timber producers, and given this background, I can only assume some sort of industry connection or knowledge that has led to these Estonian funds making a concentrated bet on AEP.

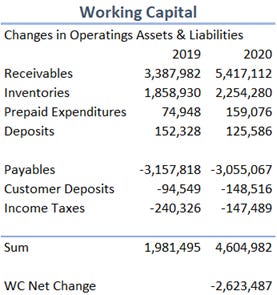

Working Capital

My working capital definition is current operational assets minus current operational liabilities, excluding items like cash, debt, and financial investments as these not related to current operations.

A significant negative change in working capital was recorded year over year. This is potentially concerning, representing a failure of the company to timely collect receivables owed. At the same time, owing to the extraordinary pandemic context and its impact on small business owners, contractors, and builders, some of these may have simply been delayed due to the inherent uncertainty of what the future would look like after or at time of order.

Remember that revenue in 2019 and 2020 was relatively constant. A significant negative change in working capital would be a problem in a normal operating environment, but here I am at least temporarily less concerned. I do, however, need this to decrease going forward or else my concern over the viability of future cash flows will grow.

Below we can see the increase in trade accounts receivables, net of loss allowances. Notice how past dues in 2020 are significantly higher than in 2019.

Cursory research into the impact of the pandemic on construction demonstrates that the pace of construction slowed dramatically as workers were issued stop work orders and forced to socially distance on site. In practical terms, builders who put in orders to AEP for engineered materials have had to delay payment to AEP as they have had to reset their building schedules, hence their own ability to collect payment. AEP has had to invest cash up front to build these orders, with receivables in limbo, waiting to be paid in cash.

While I am wary of overly rationalizing the impact of pandemic on AEP’s cash flows, I believe this to be accurate. For now, I am not too concerned, but I will be watching this closely. If I am wrong, and the growth of accounts receivables is not arrested soon, then future cash flows will suffer as AEP is forced to write off uncollectable accounts.

Impact of Lumber Prices on Revenues

Everyone and their dog are talking about the obscene volatility in lumber prices. Lumber prices jumped more than 500% between April 2020 and May 2021 to hit an all-time high of almost $1,700 per thousand board feet on May 7th, as sawmills were unable to meet unexceptional demand for home building and DIY home improvements spurred by the coronavirus lockdowns. Lumber futures remained near $500 in the third week of July, the lowest in a year, as demand normalizes while mill production has rebounded as the labor-related issues from the pandemic dissipate.

In September 2020, AEP’s CFO said the following:

“We are anticipating some negative impact with the increasing lumber prices as they are rising substantially in comparison to prior years. Our operations have been diligently increasing the pricing in our design and quoting software in order to mitigate the rising prices as much as possible. There are orders that were taken prior to rising lumber prices and those are still be honored, but where possible we are re-quoting. In addition, our Vendor Managed Inventory system that we have at all of our locations for lumber has created a delay in seeing the substantially increasing lumber prices on our supplier invoices. Our lumber supplier stocks our yard with lumber based on our usage and needs that they have purchased already. Some of that stock, which was received in our yard when prices were lower, may take our locations a few months to work through before the location starts to use higher priced lumber.”

While a rise in lumber prices may bump revenue, profit margin improvement over the next year is key here. My hope is that the rapid upwards movement in lumber prices has been balanced out by the equivalently rapid down movement since the peak in May. The struggle with a business like this, excessively reliant on a singular commodity input, is their ability to quote and pass on prices increases/decreases fast enough to retain profitability on the way down and a competitive edge on the way up.

At the end of the day, AEP does not necessarily benefit from rising lumber prices, especially if previous contracts were priced according to now expired commodity prices. Supply disruptions and rising prices likely reduced the total volume of product sold, impacting organic growth. This has been perfectly transitory, however, and a return to less volatile conditions will see AEP do better through end of 2021. Full granularity of this extreme lumber volatility event will not be available until after Q2 earnings.

Debt & Equity

The first and second BDC loans consist of term loans bearing interest at a floating base rate at 6.10% and 7.64%, due in June 2040 and June 2027, respectively. The TD term loan is at a fixed rate of 2.19% with maturity in December 2027. Nothing special to see here. I believe AEP is sufficiently capitalized to handle its long-term debts.

Equity is mostly tangible, with current assets plus plant, property and equipment making up more than two thirds at almost $20 million. Intangible assets are goodwill and other, such as customer relationships, brand, certifications and non-compete agreements.

At a current market cap of $21 million, you can buy the business today at no premium to tangible value.

A Note on Canada’s Housing Environment

Residential building costs have skyrocketed across Canada this year owing to pandemic supply chain disruptions compounded by increased demand for building materials. While Canadian real estate prices continue to rise and are among the highest relative to per capita income in the OECD, nobody has any certainty about what the future holds for Canadian residential construction or real estate. Statistics Canada notes that construction costs were up for every building type in the first quarter of 2021, ranging from a 1.2% increase for office buildings, to a 6.9% gain for townhouses, followed closely by a gain of +6.8% for single-detached houses.

It is worth noting that Canada’s national housing agency, the CMHC, projected an imminent correction at the onset of the pandemic in March 2020. As of March 2021, prices were up 31% year-over-year and have only been rising higher since. Toronto and Vancouver now rank as some of the most unaffordable cities to live in the world. Tyrannical zoning and NIMBY sentiment is mostly the reason for this. For instance, a mind boggling 80% of metro Vancouver is exclusively zoned for single family dwellings.

I believe that renewed investment in increasing housing supply, specifically multifamily residential mixed-use, will be key to the prosperity of Canadians seeking to live in urban centers. Canadian cities, like their American counterparts, are infamous for their car centric development and endless suburban sprawl.[1] Sustainability issues aside, this form of low-density urbanism is simply not life affirming. I would love to see Vancouver and Victoria take on a more Berlin/Copenhagen vibe, but for now, maybe I am dreaming.

[1] Except Montreal and Quebec City, as these were fortunate enough to develop long before hegemony of the automobile.

Any update on your thesis with AEP?